Launched 14th of September 2019, the European Second Payment Service Directive (PSD2) has now been in place for more than three years. Time for ndgit to have a look at the statistics, insights and outlooks of its PSD2 solution with the usage from Europe’s major banks in 36 productive instances and eight countries in EU and UK.

Facts & figures of PSD2 after three years of practice

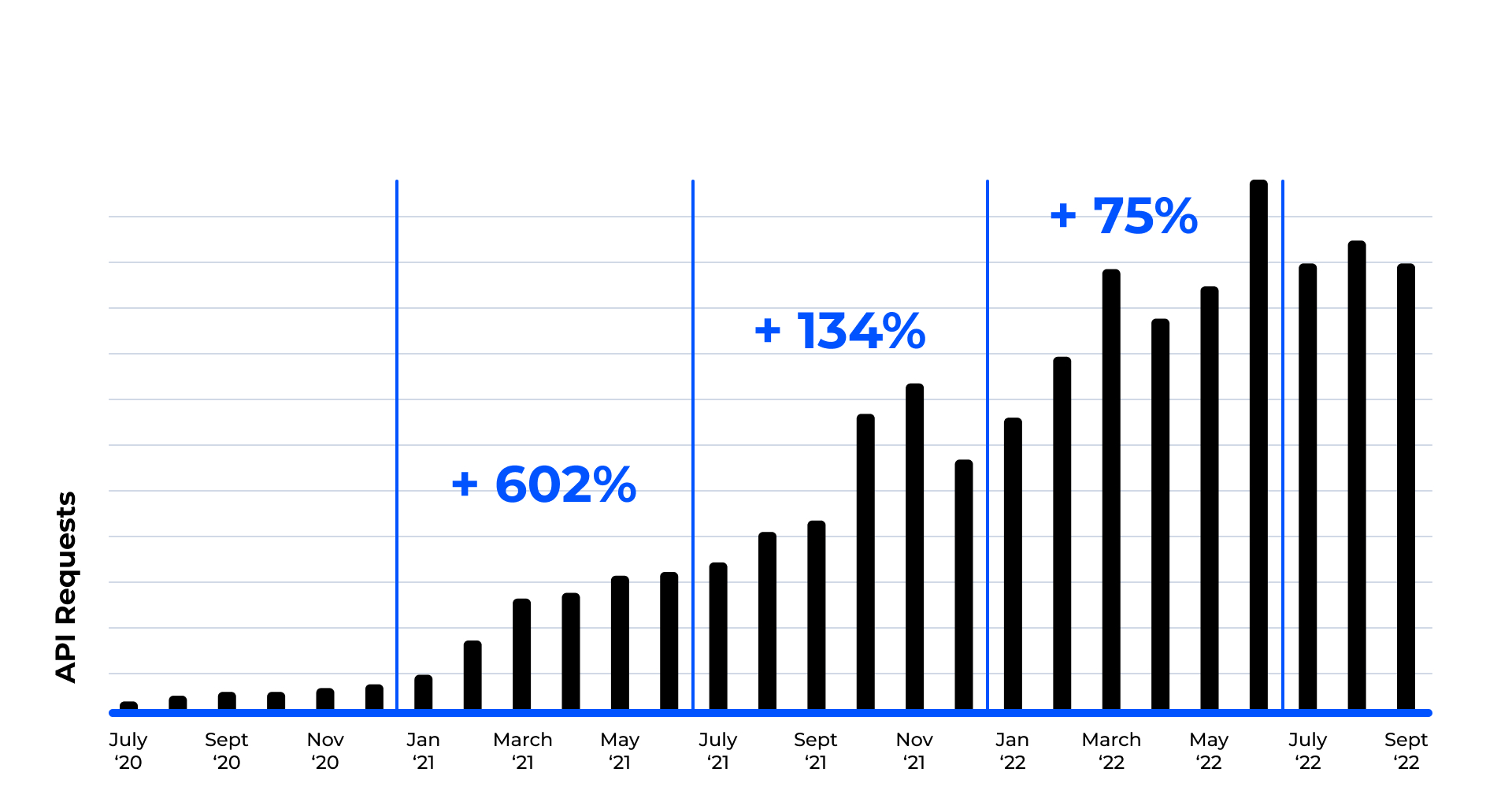

75% growth of PSD2 API usage in H1/2022

PSD2 API usage is growing with new upcoming users and increasing usage of TPP products. This shows a still existing hunger for Open Banking.

Having had 602% growth of PSD2 API requests in H1/21 and 134% in H2/21, the development continued with 75% growth in the first half of 2022. We assume this to come from an increasing number of established PSD2 use cases and a growing demand of end-customers for the new services.

Steadily growing API requests on the production systems of our customers

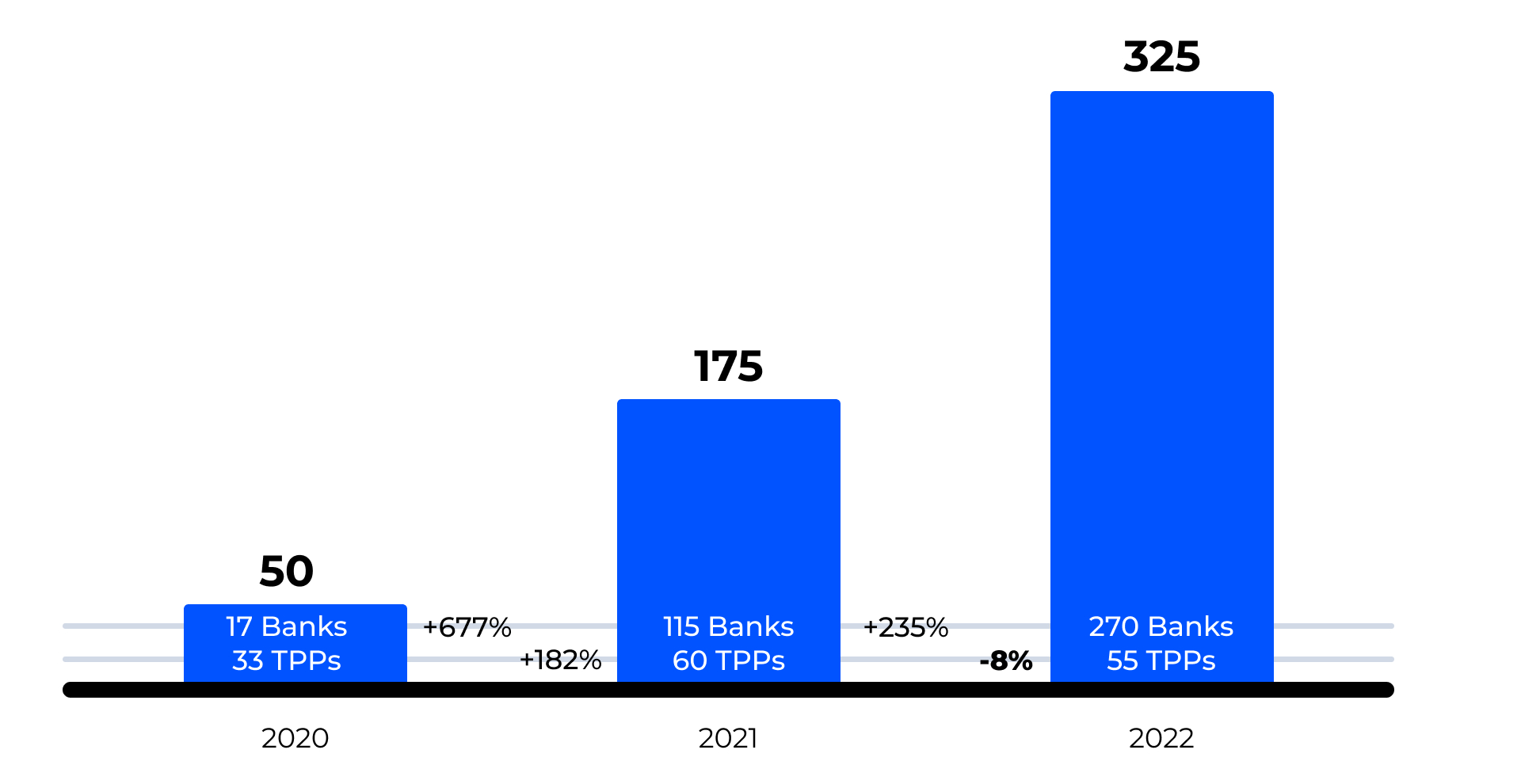

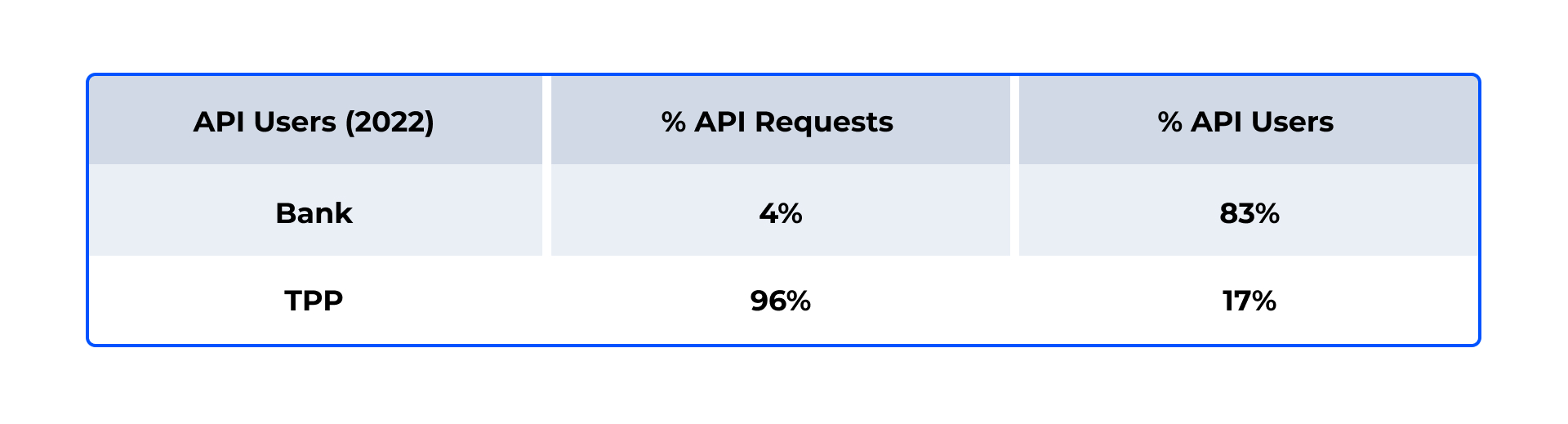

86% increase of third parties (PSD2 API users) in 2022 mainly driven from banks

While 83% of PSD2 API users are banks, TPPs/ non banks are initiating 96% of the API-requests. This indicates that TPPs still have the more mature PSD2 use cases.

Active PSD2 API users on production increased especially on the bank side

After a strong increase of accessing API users of 250% in 2021, the growth continued with 86% in 2022 (until eoQ3). While the growth in 2022 was mainly driven by the number of requesting banks coming to a total of 270, they only contribute 4% of API traffic. On the other side the number of TPPs declines to 55 but origin 96% of the PSD2 API requests. We assume that we can see that banks are only experimenting with few use cases like multi-banking while the TPPs have the more mature models on their side. The decline of TPP can also be a first sign for a consolidation in the TPP market.

Distribution of accessing API users and their associated API traffic for 2022 (until eoQ3)

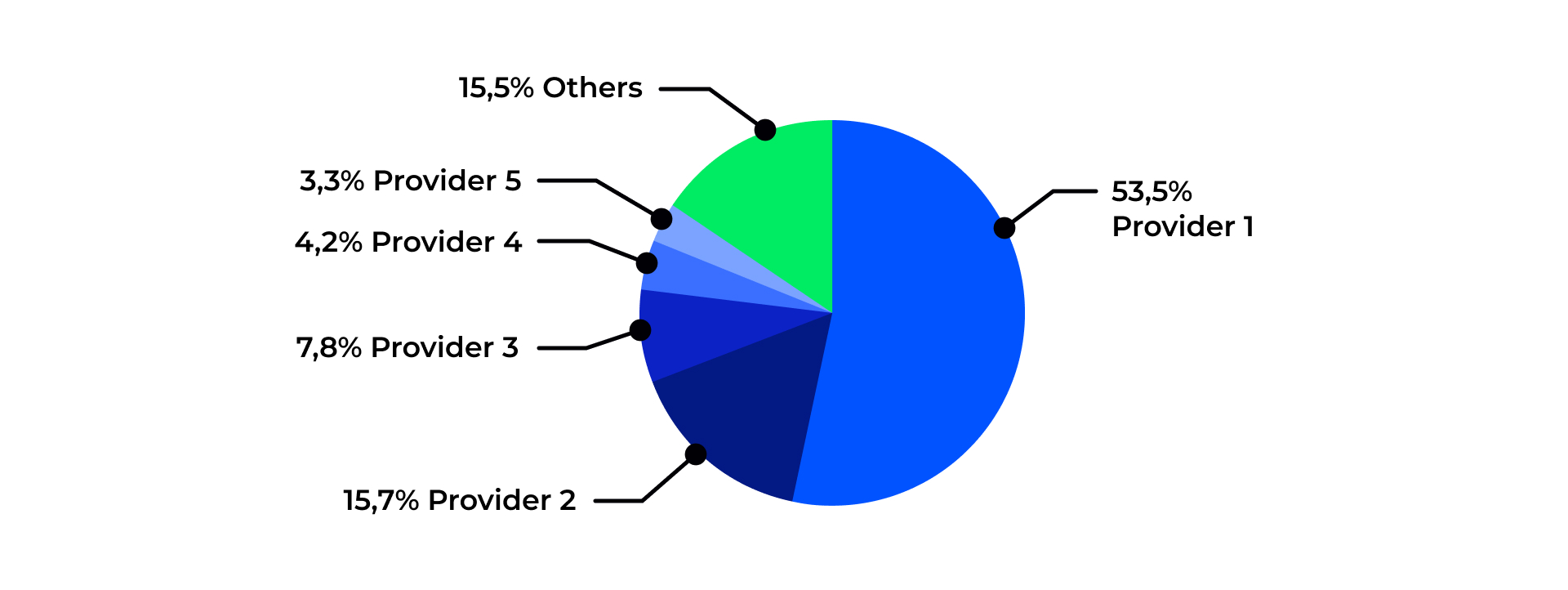

Top 10 PSD2 API users initiate 92% of the traffic.

Most of PSD2 API requests are coming from few users with two TPPs being far beyond all others. This can also be a sign of a consolidation in the commercial use of PSD2 APIs.

While the Top 10 PSD2 API users cause 92% of the traffic, we can further see a stable growth among the top five PSD2 API users which are all non-bank but only the two top TPP have a significant development over time. We see this as an indicator for a selection of PSD2 business models ending up with few TPPs having a mature proposal and a broad end-customer demand.

The distribution of API requests per top 5 API users in 2022 (Q1-Q3)

92% of PSD2 API requests affect Account Information Services (AIS)

By far the most used PSD2 service is AIS, while Payment Initiations services (PIS) are much less relevant. For confirmation of funds (FCS) there seems to be no practice relevant use case as of today.

AIS is with 92% of all API requests by far the most used service also having a constant growth, for PIS there is only slight increase from few players while FCS s hardly used at all with a total of 150 API requests in 2022. This indicates that the idea of the need of a funds confirmation service for payment instrument issuers did not come true.

The distribution of API requests per API service

Updates from the PSD2 Regulation

Mandatory SCA Exemptions

A new adjustment of EBA’s RTS has now been published in the Official Journal of the EUon the 5thof December 2022 andforces banks to change or extend their strong customer authentication capabilities andthus support SCA exemptions.

SCA exemptions become mandatory for AIS use cases together with some pre-conditions.

The period after which an SCA for AIS has to be renewed prolongs from 90 to 180 days.

The change is reasoned with the inconsistent application of the exemption across the market resulting in frictions for TPPs and end-clients. Clients of ndgit will be able to realise the change of their PSD2 APIs with our product by adjusting the configuration, enabling recurring consents and allowing for account access of 180 days.

Names of Account Owners and Users

Update on the latest Berlin Group PSD2 API specification change from 1st July 2022 now allowsbanks to provide TPPs with ‘account owners’ and ‘usernames‘ in some cases.

The EBA clarified in a multi-stage Q&A on its website that banks need to provide the same information in AIS and PIS use cases to the TPPs as the end-customer might see in his digital banking. This includes the name of the user who executed the use case and did SCA, e.g. an employee or authorised signatory. Based on this, Berlin Group published an extension in Version 1.3.12 to return PSU (payment service user) names besides the account holder names. Clients of ndgit PSD2 Compliance will receive the according feature with the next release.

From PSD2 to PSD3?

PSD2 is evolving as European Commission made consultations on the PSD2 success to identify open issues and amendments. TPPs and banks can prepare their minds on future adjustments.

European Commission conducted their consultations on the PSD2 from May until August 2022. Besides (1) a targeted consultation on the review of PSD2 from professional stakeholders there was also (2) a public consultation on the application and impact of PSD2 addressing the general public and a broad range of stakeholders. In addition, the EU Commission also started (3) the targeted consultation on Open Finance to get a better understanding of the public views on Open Finance market developments, user needs and possible future adjustments. Reactions and results from the EU commission with amendments or a path to a PSD3 are expected for 2023.

about ndgit

ndgit is an Open Finance pioneer and supports many of Europe’s major banks to open-up and connect their banking systems via PSD2 APIs to TPPs. The PSD2 Compliance software of ndgit is a standard SaaS solution which covers the regulatory PSD2 API requirements towards banks in a highly efficient and secure way. It supports the most established Berlin Group standard as well as all regulatory requirements of the EBA. The feature set can be modularly configured to the requirements of a bank and is extendable for future Open Finance solutions. More than 30 banks in Europe like BAWAG, Credit Suisse, Solarisbank, UBS or Volkswagen Financial Services implement their PSD2 APIs with ndgit.

The Payment Services Directive PSD2 came into force on 14 September 2019, with the aim of improving consumer protection and the security of electronic payments. The regulation also aimed to promote competition on the one hand, and innovation on the other. In 2022, the European Commission put PSD2 to the test. To this end, there […]

According to analysts, we may expect a continued strong growth for the open banking market. Thus, the global open banking market size will reach $135.17b by 2030, meaning a CAGR of 26.9%. Drivers of the expansion are the rise of open APIs, an increased adoption of innovative applications and services and the favorable government legislation. […]

The largest European online car market, AutoScout24, enters the B2B business. With the purchase of AUTOproff, the leading European B2B marketplace for car dealers, Autoscout24 gains access to more than 43,000 dealers across Europe and opens up a completely new business area. More than 20,000 registered car dealers can buy and sell vehicles in real […]

Next level embedded finance platforms: From regulatory-driven to market-driven Open Banking infrastructure The introduction of PSD2 has put pressure on banks to implement the Payment Service Provider Directive by the deadline of early 2018. The result was a boom for service providers specialising in the management of PSD2-relevant interfaces (APIs). Ndgit thus made it into […]

Open Banking 2022: Trends in Business and Technology* (*Webinars only available in German) In 2021, the digitization of the banking world will accelerate significantly once again. In our webinars, we want to show what opportunities banks have to leverage this development for their business: both in the form of more efficient technological solutions and through […]

Working with an external PSD2 API solution provider can have various benefits: reducing costs and risks on the one hand and opening new business opportunities through enabling new business models or external service offerings by TPPs on the other hand...

As a software development company for Open Banking cyber security is critical for us and our customers. Therefore, a strategic approach is mandatory to achieve the right maturity level. The first step is to organize a security strategy that prioritizes cybersecurity as a company imperative.

ndgit announced today that the leading provider of market research and analysis on information technology, Forrester Research, has included ndgit among the nine providers that matter most in their report, „The Forrester New Wave™: Open Banking Intermediaries, Q1 2021“.

In 2021, the digitization of the banking world will accelerate significantly once again. In our webinars, we want to show what opportunities banks have to leverage this development for their business.

Banks need to open up their backend systems and connect with third-party providers. Roger Wisler, Business Manager Switzerland at ndgit, reflects in a blog post about the core aspects of opening up banks as well as on the latest developments in Switzerland.

Over the past 18 months, one topic or acronym has been the main concern of the banking industry: PSD2 or tendered Payment Service Directive II. Driven by legal requirements, banks had to develop strategies and solutions to open their systems to third party providers [...]

Guest article - By Oliver Bohl and Birgit Spors, Advanced

What role does invisibility play for banks – especially in the area of tension of the platform economy? Today, established portals increasingly dominate customer perception. Mediated or integrated services of third parties lose their anchor point in the customers' consciousness. Are these developments a trap for banks or rather an opportunity?

Not all, but many, traditional banks are very busy with themselves. As a result, they’re often too distracted to confront external disruptors. It also means there's little time or consideration for their own disruptive evolution. There are just too many other things to tackle first.

Interesting interview between the Austrian online magazine economy.at and our CEO, Oliver Dlugosch, about Open Banking as a challenge to time-honoured financial institutions, current industry trends and his experience as FinTech entrepreneur.

Nils Elmark discusses the disruption in the banking environment and explains why financial executives must have bigger dreams. "They have to forget the past and leave the old business models behind and instead take the new FinTech and InsurTech tools on an adventure."

Banking disruption forces banks to adapt to new technologies, with voice banking playing an increasingly important role. Voice banking may be the future and will change the financial sector permanently, but it also imposes new requirements on the IT security of banks.

Lending money can be complex and expensive for financial institutions, which face strict compliance and transparency rules (many of which were introduced following the financial crisis over a decade ago). While digitisation could make life easier, its progress is often stalled in operational silos with change viewed by various bank departments as a threat rather than an opportunity.

Kevin Smith is Head of Analytics & AI at Contovista. As a data scientist, Kevin Smith specialises in analysing data using AI methods and extracting actionable insights from it. In this interview, he answers three questions about the opportunities that data-driven banking affords for medium-sized banks.

Currently, everyone is talking about Open Banking. One important thing is the right definition or interpretation of this term. There are some banks that understand Open Banking as purely publishing OpenAPIs so TPPs can access their data. But Open Banking is so much more than this...

In an exclusive interview with Money Today in Switzerland, ndgit’s CEO, Oliver Dlugosch, and Head of Business Development, Franziska Zangl, share their thoughts on PSD2 toolkits, the importance of open banking and the role of Swiss banks.

European banks are increasingly discovering the power of going beyond PSD2 and successfully advancing their open banking projects. Here, Peter Hiekmann, of ndgit, looks at how Middleware and APIs are linking banks and FinTechs to power next generation Platform Banking and accelerate a brave new world of financial services.

PSD2 is a starter drug for many into open banking. PSD2 means implementing a software that follow all PSD2 rules i.e. an out-of-the-box solution from providers like ndgit.

PSD2 and Open Banking have paved the way for banking transformation. But compliance and regulation aside, what else is driving change, how should banks respond and how does this impact their service direction?

Ensuring seamless consent management is a cornerstone of PSD2 implementation. Here, Oliver Dlugosch, CEO of ndgit, explains how dedicated APIs can help banks reduce complexity and make processes smoother.

While current guidelines necessitate Two-Factor Authentication, some transactions are exempt. Oliver Dlugosch, CEO of ndgit, clarifies the secure ‘rules of engagement’ for Banks and Payment Service Providers.

In 2018, PSD2 effectively lit a touch paper to wholescale Banking transformation. It may be a slow burn but, according to Oliver Dlugosch, CEO of ndgit, it’s already generated far-reaching changes to investment attitude and strategy.