European banks are increasingly discovering the power of going beyond PSD2 and successfully advancing their open banking projects. Here, Peter Hiekmann, of ndgit, looks at how Middleware and APIs are linking banks and FinTechs to power next generation Platform Banking and accelerate a brave new world of financial services.

PSD2 and Open Banking have been on European bank agendas since the second European Payment Services Directive came into force in early 2018. For the first time, we have a legislature that touches banking’s core products and challenges its sovereignty over bank data.

Owning customer account data has long given banks a competitive edge, for example in terms of pricing and product selection. This competitive advantage is now shrinking as third-parties gain access to bank accounts in order to provide consumers with innovative value-added banking services.

The result? Classic revenue models for banks are breaking away and customer relationships are starting to erode.

Radical departures from traditional banking models

While some banks bemoan the demise of traditional banking, others are embracing change and are showing the first flush of success. This includes using their digital platforms to create ‘financial supermarkets’ for users.

For example, Deutsche Bank, is developing its “DB API” interface program as a one-stop-shop that will provide all services relevant to the customer in a complete 360° view. (Imagine classic networked banking with additional functions like accounting, evaluations, personal finance management, etc.)

A similar approach is being taken by the Dutch ING, the Spanish BBVA and the Northern European Nordea. In addition, almost all Swiss banks, although not “PSD2-liable”, are advancing their implementation of Open Banking.

Middleware freeing up core banking systems

There is no arguing the virtually unlimited opportunities for open banking. The challenge is technically enabling them.

Here, APIs hold the key to linking open financial architectures. They help to overcome the integration challenges associated with connecting core legacy systems’ heterogeneous architecture, creating new pathways for it to be “opened” up to a broader and more diverse product, service and ecosystem.

This is done by adding a middleware layer onto the existing core banking system.

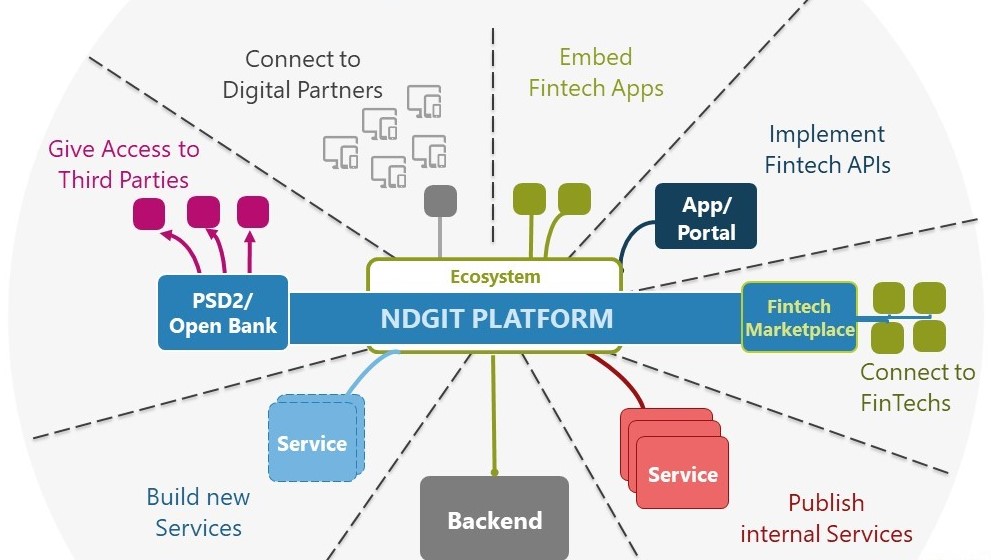

Often provided by technical service providers such as ndgit, this serves to dock, control, and evaluate FinTechs via APIs. (See diagram below)

Delivering faster & easier compliance

For many banks, platform banking is the ideal implementation path to PSD2 compliance. Predeveloped and standardised ‘PSD2 Ready’ software can be installed at the participating bank to ensure APIs are successfully integrated to the secure connection of third-party providers and to automate all necessary reports.

Moving beyond this, APIs can open up the core banking system for the central connection of all digital channels – from e-banking via convenient REST interfaces for third-party providers to internal consultant applications.

Creating easy access and multiplication of services

The central component of this is the API Gateway. The gateway controls the secure access of internal and external partners and manages all accessing applications centrally.

To quickly and easily integrate customer innovations and FinTech services into their API management platforms, banks are either building their own network or leveraging marketplaces provided by bridge builders like ndgit. This helps them create a virtually future-proof platform where various FinTechs and forms can be connected in a self-contained ecosystem that uses the bank as “hub”.

A good use case is using an API platform to digitise the lending process. A car loan could be fully digitally approved in just a few minutes using XS2A PSD2 Compliance, Account Analytics, Credit Ratings, Digital Signature, and Video Legitimation APIs to provide the lender with all the data they need to make a decision on the applicant’s creditworthiness and to sign a legally binding contract. All actioned without creating unnecessary friction for the customer.

Moving from products to platforms

In almost all areas, companies are increasingly switching from products to platforms, thereby changing the entire market, especially for established market participants.

A glimpse into the recent past of other industries, such as telecommunications, shows the significance of this: Nokia and Blackberry are now a shadow of their former glory, their technology and products supplanted by Apple and the Android ecosystems. Here, triumph was less about operating functions than the thousands of different features and programs available from the App Store, where external developers create value for the end customer.

Within banking, the rise of platforms is largely driven by three technologies; the cloud as a permanent storage location; global networking through social apps; and mobile, which brings banking to where the customer needs it.

To transform their products into platforms banks must look really closely at whether their strategy aids development in these key areas:

Connectivity: How easily can services be integrated in the backend?

Attraction: How strong is the attractiveness of the platform for participants – both service providers and consumers

Ecosystem: To what extent does the platform promote exchange and shared value creation?

The following diagram shows how ndgit enables platform based Open Banking and Digital Ecosystems.

Pioneers are already accelerating success

Banks must begin to accelerate their Open Banking technology now or risk getting left behind. Already we are seeing forward-thinking banks coming to market with solutions that will fast track them on the road to success.

A great example of this is Hypothekarbank Lenzburg’s (HBL) Open Banking project, which shows how a platform can be realized in a short time and using an existing IT system. This enables FinTechs and other partners to retrieve their data about HBL’s banking products via standardized APIs and trigger customer-related processes in the bank. HBL has now connected its own digital ecosystem and numerous FinTechs, including Neon and Contovista.

As the first bank in Switzerland, HBL is now able to offer customers attractive added-value services, thus increasing customer loyalty and generating additional revenue through commissions from the affiliated FinTechs. The interface platform, which is based on the core banking system of HBL, comes from ndgit, Europe’s number one provider for API platforms.

This past year has shown that, whether investing in new technology or using APIs and middleware to achieve more with what they already have, more banks are placing Banking as a Platform at the top of their agenda. Signifying beyond doubt that the Open Banking financial revolution is not just gaining momentum but is already accelerating the transformation of banking models and services forever.

This article is an excerpt from the topic dossier “Mit der Plattform ins neue Banking-Zeitalter” (German) of the Bankenforen. Download the complete Bankenforen dossier (German) here.

Launched 14th of September 2019, the European Second Payment Service Directive (PSD2) has now been in place for more than three years. Time for ndgit to have a look at the statistics, insights and outlooks of its PSD2 solution with the usage from Europe’s major banks in 36 productive instances and eight countries in EU […]

According to analysts, we may expect a continued strong growth for the open banking market. Thus, the global open banking market size will reach $135.17b by 2030, meaning a CAGR of 26.9%. Drivers of the expansion are the rise of open APIs, an increased adoption of innovative applications and services and the favorable government legislation. […]

The largest European online car market, AutoScout24, enters the B2B business. With the purchase of AUTOproff, the leading European B2B marketplace for car dealers, Autoscout24 gains access to more than 43,000 dealers across Europe and opens up a completely new business area. More than 20,000 registered car dealers can buy and sell vehicles in real […]

Next level embedded finance platforms: From regulatory-driven to market-driven Open Banking infrastructure The introduction of PSD2 has put pressure on banks to implement the Payment Service Provider Directive by the deadline of early 2018. The result was a boom for service providers specialising in the management of PSD2-relevant interfaces (APIs). Ndgit thus made it into […]

Open Banking 2022: Trends in Business and Technology* (*Webinars only available in German) In 2021, the digitization of the banking world will accelerate significantly once again. In our webinars, we want to show what opportunities banks have to leverage this development for their business: both in the form of more efficient technological solutions and through […]

Working with an external PSD2 API solution provider can have various benefits: reducing costs and risks on the one hand and opening new business opportunities through enabling new business models or external service offerings by TPPs on the other hand...

As a software development company for Open Banking cyber security is critical for us and our customers. Therefore, a strategic approach is mandatory to achieve the right maturity level. The first step is to organize a security strategy that prioritizes cybersecurity as a company imperative.

ndgit announced today that the leading provider of market research and analysis on information technology, Forrester Research, has included ndgit among the nine providers that matter most in their report, „The Forrester New Wave™: Open Banking Intermediaries, Q1 2021“.

In 2021, the digitization of the banking world will accelerate significantly once again. In our webinars, we want to show what opportunities banks have to leverage this development for their business.

Banks need to open up their backend systems and connect with third-party providers. Roger Wisler, Business Manager Switzerland at ndgit, reflects in a blog post about the core aspects of opening up banks as well as on the latest developments in Switzerland.

Over the past 18 months, one topic or acronym has been the main concern of the banking industry: PSD2 or tendered Payment Service Directive II. Driven by legal requirements, banks had to develop strategies and solutions to open their systems to third party providers [...]

Guest article - By Oliver Bohl and Birgit Spors, Advanced

What role does invisibility play for banks – especially in the area of tension of the platform economy? Today, established portals increasingly dominate customer perception. Mediated or integrated services of third parties lose their anchor point in the customers' consciousness. Are these developments a trap for banks or rather an opportunity?

Not all, but many, traditional banks are very busy with themselves. As a result, they’re often too distracted to confront external disruptors. It also means there's little time or consideration for their own disruptive evolution. There are just too many other things to tackle first.

Interesting interview between the Austrian online magazine economy.at and our CEO, Oliver Dlugosch, about Open Banking as a challenge to time-honoured financial institutions, current industry trends and his experience as FinTech entrepreneur.

Nils Elmark discusses the disruption in the banking environment and explains why financial executives must have bigger dreams. "They have to forget the past and leave the old business models behind and instead take the new FinTech and InsurTech tools on an adventure."

Banking disruption forces banks to adapt to new technologies, with voice banking playing an increasingly important role. Voice banking may be the future and will change the financial sector permanently, but it also imposes new requirements on the IT security of banks.

Lending money can be complex and expensive for financial institutions, which face strict compliance and transparency rules (many of which were introduced following the financial crisis over a decade ago). While digitisation could make life easier, its progress is often stalled in operational silos with change viewed by various bank departments as a threat rather than an opportunity.

Kevin Smith is Head of Analytics & AI at Contovista. As a data scientist, Kevin Smith specialises in analysing data using AI methods and extracting actionable insights from it. In this interview, he answers three questions about the opportunities that data-driven banking affords for medium-sized banks.

Currently, everyone is talking about Open Banking. One important thing is the right definition or interpretation of this term. There are some banks that understand Open Banking as purely publishing OpenAPIs so TPPs can access their data. But Open Banking is so much more than this...

In an exclusive interview with Money Today in Switzerland, ndgit’s CEO, Oliver Dlugosch, and Head of Business Development, Franziska Zangl, share their thoughts on PSD2 toolkits, the importance of open banking and the role of Swiss banks.

PSD2 is a starter drug for many into open banking. PSD2 means implementing a software that follow all PSD2 rules i.e. an out-of-the-box solution from providers like ndgit.

PSD2 and Open Banking have paved the way for banking transformation. But compliance and regulation aside, what else is driving change, how should banks respond and how does this impact their service direction?